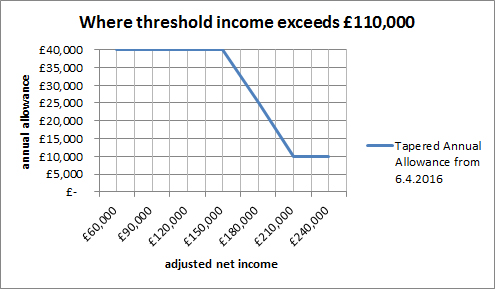

Following announcements in the July 2015 Budget, from 6th April 2016 there will be a tapering of the Annual Allowance for those with adjusted net income (including personal and employer contributions) of £150,000 or more. In these cases, the normal annual allowance will be reduced by £1 for each £2 of income above £150,000 subject to a maximum reduction of £30,000 for those earning £210,000 or more.

What this means in practice:

Firstly, in order to work out whether tapering applies you need to establish two values – “threshold income” and “adjusted net income”. It makes sense to start with threshold income:

This is the total amount of earned and investment income, and as such includes:

It excludes pension contributions, other that salary exchange arrangements put in place on or after 8th July 2015.

If the total of the above is less than £110,000 then the tapering of the annual allowance does not apply.

This is the same as threshold income (above) PLUS the gross value of personal contributions made under net pay schemes plus any employer contributions (whether by salary sacrifice or not).

If threshold income is above £110,000 and the value of adjusted net income exceeds £150,000 then then tapering of the annual allowance will apply at the rate of £1 reduction in the annual allowance for every £2 the adjusted net income exceeds £150,000. The amount of the reduction is rounded up to the nearest whole pound, and is subject to a maximum reduction of £30,000 (for those with adjusted net income of £210,000 or more).

Individuals in receipt of higher income should speak to their financial adviser and accountant to see whether they are affected by this. For some, it may not be obvious whether the limits will be exceeded until after the end of a tax year, making planning more challenging.

Carry forward is still available for those subject to the tapered annual allowance.

Tapering does not affect the Money Purchase Annual Allowance, but it will reduce the “alternative annual allowance” which can apply for individuals who have accessed some of their pension savings under the new flexible options and who are accruing benefits in a Defined Benefits scheme. The “alternative annual allowance” is normally £30,000 but can be reduced by tapering.

The tapering of the annual allowance is dealt with through your tax return, there is no need to tell us although customers should always discuss this with their financial adviser.

March 31st, 2016

The Minerva SIPP can invest in a wider range of assets including commercial property and land, on an individual or group basis. Any combination of permitted investments may be made within a Minerva SIPP including deposit accounts, DFM, open market platform/wrap accounts, stockbroker accounts and trustee investment plans, all held together within the same SIPP.

SIPP Lite is a lower cost option, for those that do not require multiple investment accounts, or access to commercial property and land at outset. SIPP Lite members are restricted to a maximum of one investment account, to run alongside the default SIPP bank account. This investment account could be another bank account or ONE of the following: stockbroker account, DFM, open market platform/wrap account or a trustee investment plan. For individuals that require additional investments at a later date, including commercial property and land, they can upgrade their SIPP Lite plan to a Minerva SIPP.

A Small Self-Administered Scheme (SSAS) is a type of UK registered pension scheme. Each SSAS is governed by its own trust deed and rules and is a separate legal entity to the sponsoring employer. The sponsoring employer establishes the SSAS and invites members to join. Any individual employed by the sponsoring employer (or a participating employer) may join the scheme and all members are appointed as trustees alongside the professional trustee. SSAS trustees have a very wide range of investment options, including the ability to make secured loans to the sponsoring employer of up to 50% of the net asset value of the scheme, subject to certain conditions.

We have been operating in these markets for over 20 years. The SSAS business was formed in 1997, and in 2003 we launched our flagship product, the Minerva SIPP. The range is completed by SIPP Lite, which has been available since July 2012.

Read More